Invented by Edward W. Fordyce, Michelle Eng Winters, Leigh Amaro, Visa USA Inc

Intelligent analytics systems can provide valuable insights into customer behavior, spending patterns, and preferences. This information can be used by merchants to improve their marketing strategies, offer personalized promotions, and increase customer loyalty. For cardholders, intelligent analytics can help them track their spending, manage their finances, and make better financial decisions.

One of the key drivers of the market for intelligent analytics systems is the increasing use of mobile devices for transactions. Mobile payments are becoming more popular, and this trend is expected to continue in the coming years. As more people use their mobile devices for transactions, there is a growing need for analytics systems that can provide real-time insights into customer behavior.

Another factor driving the market for intelligent analytics systems is the increasing use of artificial intelligence (AI) and machine learning (ML) technologies. These technologies can analyze large amounts of data and provide valuable insights into customer behavior and preferences. AI and ML can also help merchants personalize their marketing strategies and offer targeted promotions to customers.

The market for intelligent analytics systems is highly competitive, with many companies offering a wide range of solutions. Some of the key players in the market include IBM, Oracle, SAP, and Microsoft. These companies offer a range of solutions, including cloud-based analytics platforms, AI-powered analytics tools, and mobile analytics apps.

In addition to the major players, there are also many startups and smaller companies entering the market. These companies are focused on developing innovative solutions that can provide unique insights into customer behavior and preferences. Some of these startups are using blockchain technology to provide secure and transparent analytics solutions.

Overall, the market for systems and methods to provide intelligent analytics to cardholders and merchants is expected to continue growing in the coming years. As more people use their mobile devices for transactions, and as AI and ML technologies continue to advance, the demand for intelligent analytics solutions will only increase. This presents a significant opportunity for companies that can develop innovative solutions to meet the needs of cardholders and merchants.

The Visa USA Inc invention works as follows

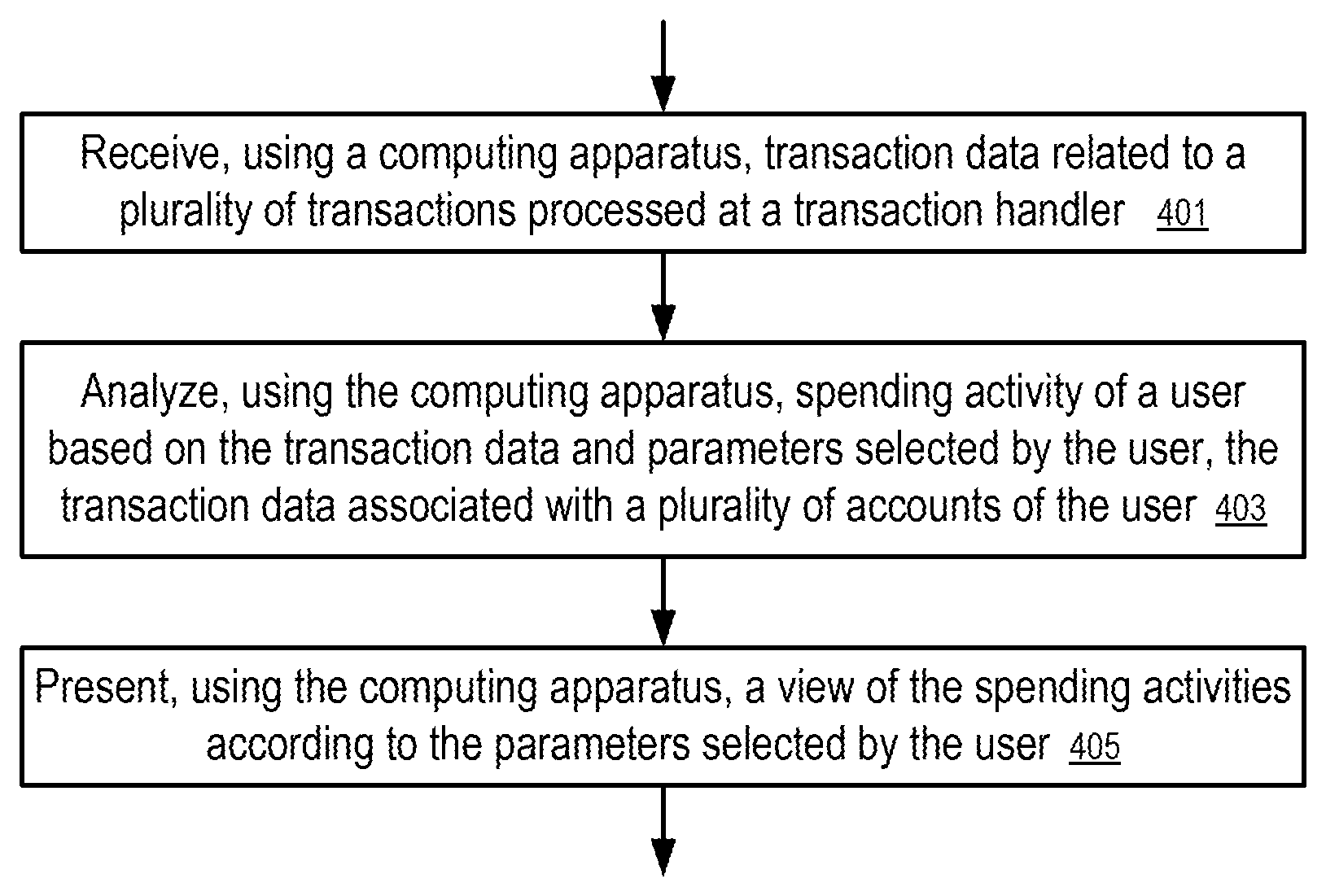

The computing apparatus comprises: a transaction processor to process transactions; a data store to record the transactions processed by a transaction handler; a portal coupled to the data store to receive input parameters and provide spending activity data for presentation in response to input parameters, and an analytics module coupled to the data storage to analyze the spending activities of a users based on transaction data and parameters and generate spending activity data regarding transactions within a plurality accounts of the user.

![]()

Background for Systems and Methods to Provide Intelligent Analytics to Cardholders and Merchants

Payment cards such as debit cards, credit cards, and prepaid cards are used by millions of people every day. The corresponding records of transactions are stored in databases to facilitate settlements and financial recordkeeping. These data can be mined for statistics, trends, and other analyses. Such data can be mined to achieve specific advertising goals. For example, to make targeted offers to account holders. No. Published on June 5, 2008, the publication is entitled “Techniques for Targeted Offers.” The publication was titled “Techniques for Targeted Offerings” and published on June 5, 2008.

U.S. Pat. App. Pub. No. No. The system discloses how a payment service can identify the activity of an online user who uses a credit card in relation to an offer that is associated with the advertisement.

U.S. Pat. No. No. 6,298,330 was issued on October 2, 2001, and is entitled “Communicating With a Computer Based On The Offline Purchase History Of A Particular Consumer.” The patent 6,298,330, issued on Oct. 2, 2001, entitled?Communicating with a Computer Based on the Offline Purchase History of a Particular Consumer,’ discloses a method in which an advertisement targeted to a particular computer is delivered in response to a cookie or other identifier corresponding to that computer.

U.S. Pat. No. No. 7,035,855, published on Apr. The patent, entitled “Process and system for integrating information from disparate databases for purposes of predicting consumer behavior”, was issued on April 25, 2006. The patent discloses a method of predicting consumer behaviour by using consumer transactional data.

U.S. Pat. No. No. 6,505,168 was issued on January 7, 2003, and is entitled “System and Method for Gathering Standardized Customer Purchase Information to Target Marketing.” The system discloses how to organize credit card, debit card, check and other purchasing information using categories and subcategories. The information about the customer’s purchases is used to create customer preferences for targeted offers.

U.S. Pat. No. No. 7,444,658, published on October 28, 2008, and entitled “Methods and Systems to Perform Content Targeting,” The patent 7,444,658, issued on Oct. 28, 2008 and entitled?Method and System to Perform Content Targeting,? discloses a method in which ads are sent to users according to a classification of the user based on credit card purchase data.

U.S. Pat. App. Pub. No. No. The patent application entitled “System and Method for Analysis of Marketing Efforts” was published on Mar. The patent application dated October 10, 2005 and entitled?System and Method for Analyzing Marketing Efforts,?

U.S. Pat. App. Pub. No. No. The patent application 2008/0217397, published on Sep. 11, 2008 and entitled?Real-Time Awards Determinations,’ discloses a method for facilitating transactions involving real-time award determinations.

The disclosures in the patent documents discussed above are hereby incorporated by reference.

Introduction

![]()

In one embodiment, the processing of transaction data (such as records of transactions via credit or debit accounts, prepaid and bank accounts, stored-value accounts, and so on) is used to provide information that can be used for a variety services such as benchmarking, advertising content, offer selection, customization, personalized, prioritization etc.

In one embodiment, an advertising network is provided based on a transaction handler to present personalized or targeted advertisements/offers on behalf of advertisers. The transaction handler or a computing device associated with it uses transaction data or other data such as merchant data or account data to generate intelligence information on individual customers or specific types of customers. The intelligence information can be used to select, identify, generate, adjust, prioritize, and/or personalize advertisements/offers to the customers. “In one embodiment, the transaction processor is further automated to charge the advertisement fees to the advertisers using their accounts in response to advertising activities.

In one embodiment, the computing device correlates transactions with events that took place outside of the context in which the transaction occurred, such as the online advertisements that are presented to customers and that, at least partially, cause offline transactions. The correlation data may be used to show the effectiveness of advertisements and/or improve intelligence about how individuals and/or different types of customers respond.

In one embodiment, the computing device correlates or provides information that facilitates the correlation of transactions with the online activities of customers, including searching, web surfing, social networking, and consuming advertising, as well as with other activities such as watching TV programs and/or events such as meetings and announcements.

In one embodiment, correlation results can be used to create predictive models that predict spending patterns or transactions based on events or activities, or to predict events or activities based upon transactions or spending patterns.

In one embodiment, the transaction handler is operated by a single entity that performs various services based on transaction data. In the case of personalized or targetted advertisements, for example, the single entity can perform operations such as generating intelligence information, selecting relevant information relevant to a particular audience, selecting and prioritizing relevant intelligence data, personalizing or generating advertisements using selected intelligence information and facilitating delivery of targeted or personalized advertisements. The entity that operates the transaction handler may also cooperate with other entities, by providing them information so they can perform some of the tasks for the presentation of personalized or targeted ads.

In one embodiment, the system comprises a transaction handler that provides a consolidated financial view with graphics, targeted offers, and content powered by data from multiple issuers.

In one embodiment, an intelligent analytics engine is used to analyze transaction data and to provide reports to both consumers and merchants.

In one embodiment, the portal provides merchants with data to help them understand customer spending habits and to create new incentives for customers. In one embodiment, the portal is used to provide consumers with targeted content and offers.

In one embodiment, the consumer is provided with an interface that allows them to enroll in a system which will collect and/or monitor transaction-related information for transactions handled by the transaction handler. The transaction handler can be configured to process payments between issuers who represent customers and acquirers who represent merchants. In one embodiment of the program, enrolling consumers allows the system not only to use transaction data to record the transactions, but to also obtain purchase details, such as stock-keeping units (SKUs) about the items purchased, receipts and warranty information from the respective merchants. In one embodiment enrollment in the program allows the system also to use related data sources which can be linked with the transaction data.

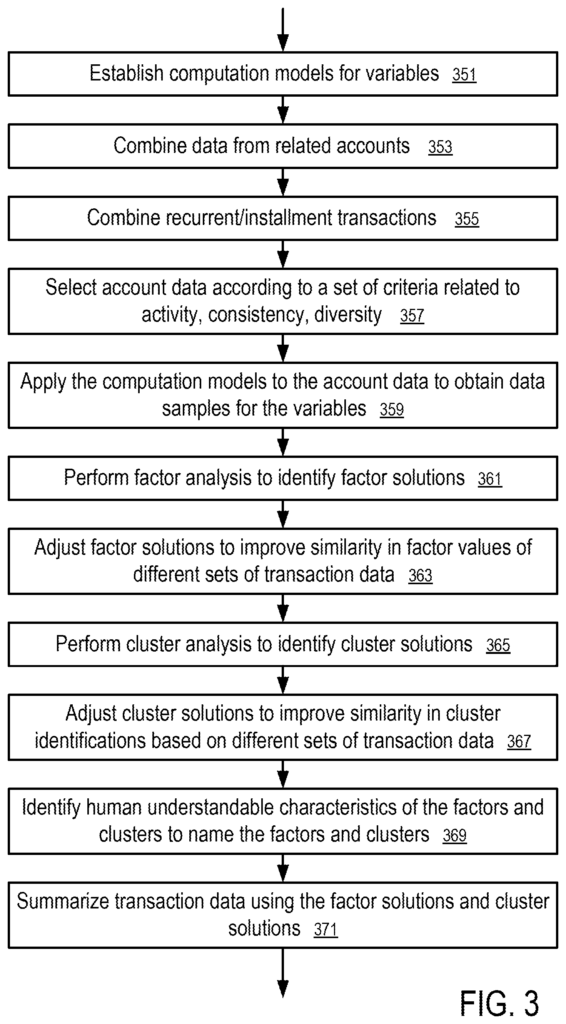

The section entitled “INTELLIGENT ANATOMICS” provides further details and examples of the transaction handler-based system, according to an embodiment.

Click here to view the patent on Google Patents.

Leave a Reply